Which professional insurance is worth considering when you’re self-employed?

Read in 3 minutes

Having your own business: it’s great to be able to do your own thing, but there are also risks associated with being self-employed. Will your business survive if you’re sick for a long period? How do you avoid having only a tiny state pension? And what if you’re expecting a baby? By setting up some safeguards or insurance, you can give yourself more security and peace of mind. Here’s an overview of the most interesting options.

Why you pay social security contributions

When you’re self-employed in a main or secondary occupation, you pay social contributions, unless you’ve been granted an exemption. These contributions are there to give you a (financial) push at various moments in your life. So in fact, you’re building up your social rights. Thanks to your contributions, you receive support from social security, for example:

- when you become a parent (i.e. the birth premium, paid maternity leave and co-parent leave, service vouchers, etc.)

- in the case of illness (i.e. benefits, exemption from social contributions, etc.)

- when caring for a close family member (i.e. benefits)

- if you go bankrupt or are forced to terminate your activity (i.e. bridging benefits)

- etc.

How do you calculate your social contributions, and what should you take into account when you start out? Read on to find out!

Becoming a parent when you’re self-employed

There are many myths about your rights as a self-employed parent. The government has made significant efforts to harmonise the rights of self-employed (adoptive) parents with those of employees.

Your pension when you’re self-employed

Let’s first clear up one thing: diligently paying your social contributions does not mean you can retire in luxury when you start claiming your pension. Fortunately, there are some tax-efficient options like the Voluntary Supplementary Pension Scheme for the Self-Employed (VSPSS/PCLI/VAPZ) to augment your savings pot.

Explore which pension savings options are suitable for you, or try our free simulator to see what your pension will look like.

Protecting yourself against loss of income

Because you pay social contributions, you also receive an indemnity from the health insurance fund when you’re self-employed. At least, if you have a doctor’s note for more than 8 days, that is. This sickness benefit is not always sufficient though, especially if the costs of your business continue. With guaranteed income insurance, you receive an additional benefit in such situations so you can keep your head above water more easily.

Income insurance is not mandatory, but it can bring peace of mind. Plus, the premiums you pay can be fully deducted from your taxable income.

Read more about guaranteed income insurance

What if you cause harm to someone or something?

You damage your client’s furniture by dropping a bucket of paint. A visitor to your sandwich shop gets sick from eating your crab salad sandwich. Accidents happen, and as an entrepreneur, your personal liability insurance is of no use in such cases. Civil liability insurance (CLI), on the other hand, will help you in situations like these.

In some cases, CLI insurance is even mandatory, for example:

- civil liability car insurance for your company vehicles

- civil liability ‘fire and explosion’ insurance for certain businesses and locations accessible to the public

Which other types of insurance are suitable when you’re self-employed?

Depending on your professional activity and personal situation, other (professional) insurance policies may also be a good idea. Industrial accident insurance is even mandatory if you work with staff. Hospitalisation insurance is useful for paying medical expenses not covered by the health insurance fund. However, this insurance is not tax-deductible.

Our advice? Have a thorough chat with your insurer, check what is mandatory, and identify which risks your activity incurs.

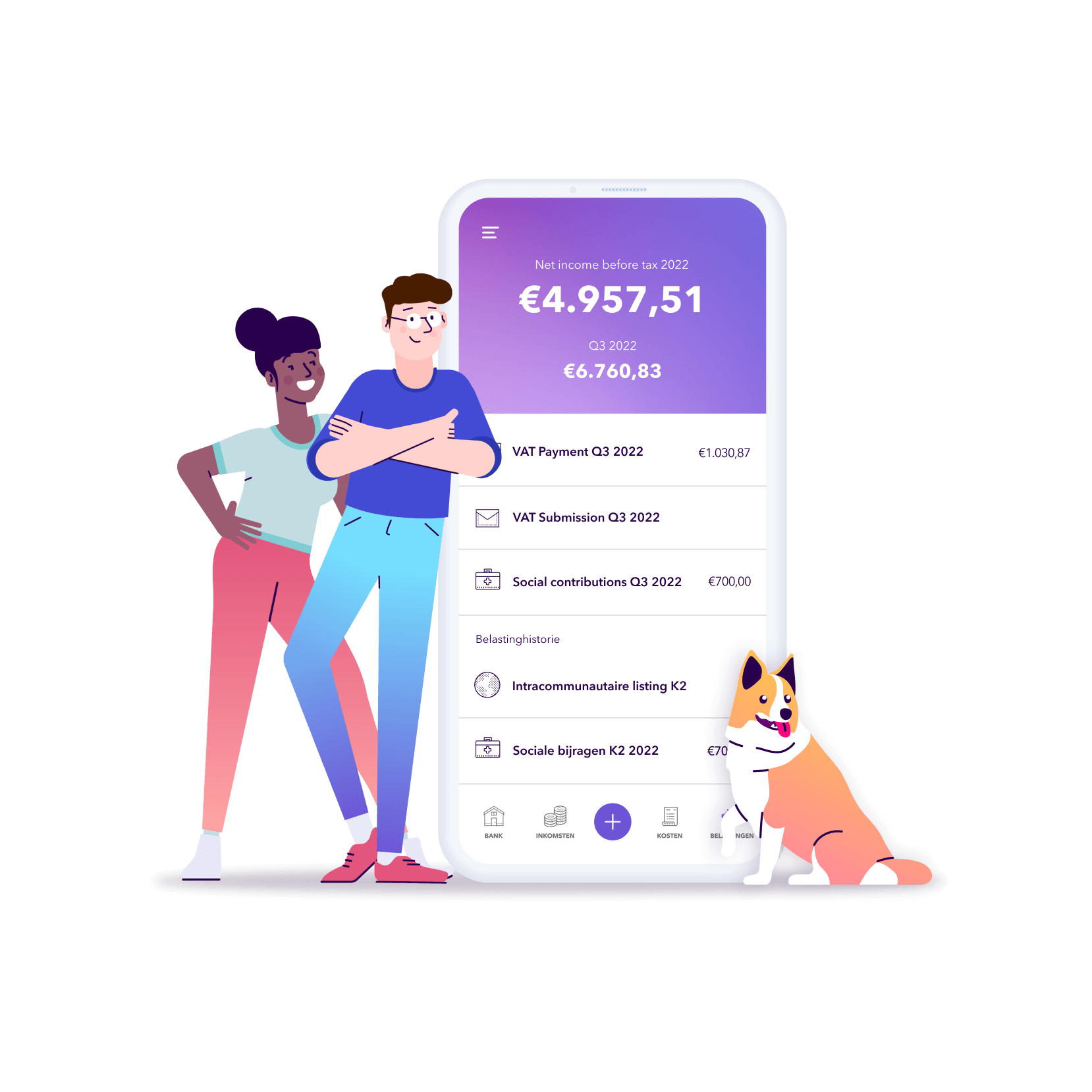

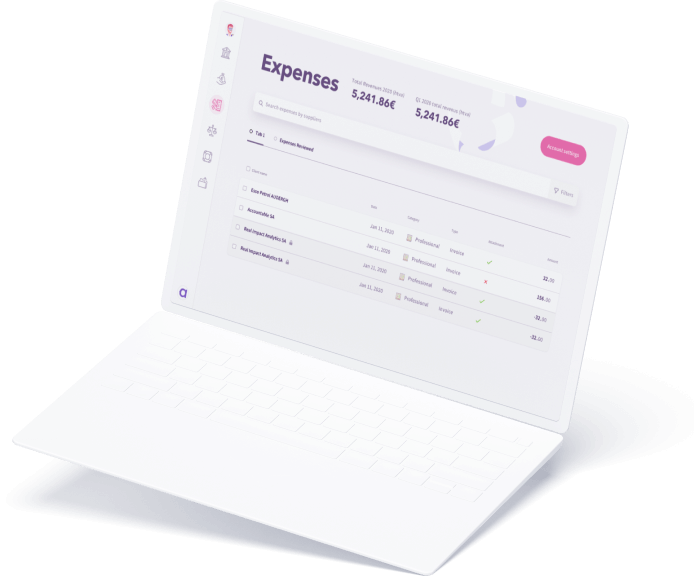

Make sure your insurance invoices and social contributions are handled correctly

Something else that gives peace of mind when you’re self-employed is always having your accounts nicely in order.

Want to easily keep track of your professional expenses and social contributions? With Accountable, you can easily upload invoices and receipts and see your paid social contributions at a glance.

Did you find what you were looking for?

Happy to hear!

Stay in the know! Leave your email to get notified about updates and our latest tips for freelancers like you.

We’re sorry to hear that.

Can you specify why this article wasn’t helpful for you?

Thank you for your response. 💜

We value your feedback and will use it to optimise our content.

What other freelancers are reading

As a Content Manager at Accountable, Valesca offers her readers an exciting and engaging content experience. Given her own experience as a freelance content marketeer & copywriter, Valesca knows the ins and outs of tax returns for the self-employed. It’s her goal to provide you with easy and understandable solutions to handle your tax returns stress-free with Accountable.